How the call centre division Closed 31% More Revenue from a Smaller Pipeline

The result we didn’t expect

For a company that built its pipeline through digital channels, a sharp drop in inbound inquiry volume triggers an immediate response: review the channels, audit the campaigns, check what changed.

We ran that review in early 2026. Nothing was broken.

What we found instead was a pipeline that had become smaller, faster, and more valuable. The buyers arriving in Q1 2026 came with defined budgets, clear vendor mandates, and short shortlists. Conversations that previously required four or five discovery calls were completing in two. Decision-makers were present from the first contact.

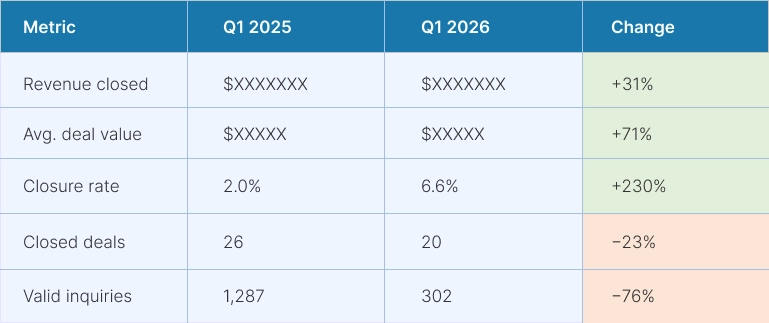

The numbers told a story we hadn’t anticipated:

Data Note: To protect proprietary business intelligence, raw volume metrics have been masked. Figures represent indexed growth of valid inbound CRM inquiries, defined by B2B decision-maker contact, established budget, and active vendor evaluation. Methodology remained constant across all compared periods to isolate shifting patterns of buyer influence over raw web traffic.”

What changed, and why

We believe the mechanism is structural rather than cyclical. Generative AI has absorbed the early research phase of the B2B buying journey. Buyers who once spent weeks building vendor understanding through search results are now arriving at that same understanding through AI-generated summaries, before they ever contact a vendor.

This is consistent with what the research shows at scale. Brands absent from AI Overviews saw organic click-through rates fall 67% through 2025 (Seer Interactive, 5.47M queries). And the majority of the B2B buying journey now occurs without vendor involvement, buyers arrive later, more informed, and with shorter shortlists than at any prior point in the digital era.

What this means for pipeline quality

The buyers who arrived in Q1 2026 were not the same profile as Q1 2025. The volume of exploratory, early-stage inquiries, buyers in the orientation phase, building their vendor understanding, fell sharply. What remained was a concentrated set of buyers who had already completed that phase.

The result: a closure rate of 6.6% against 2.0% the prior year, and an average deal value of $XXXXX against $XXXXX. The pipeline was smaller. The revenue was stronger.

This is not an argument for deliberately shrinking your pipeline. It is an observation that the top of the B2B funnel has structurally shifted, and that companies whose credibility signals are strong enough to appear in AI-generated research are increasingly the ones attracting the buyers who convert.

What we’re doing about it

Understanding this mechanism changed how we think about search and content strategy. If buyers are forming their vendor shortlist before they visit our site, the question is not how to generate more traffic, it is how to ensure we appear in the AI-generated research they are conducting before they click anything.

That means investing in the credibility signals AI models synthesise: detailed case studies with named clients and verified outcomes, third-party editorial coverage, reviews on the platforms AI cites, and named authors with verifiable expertise across the web. These are not new SEO tactics. They are the inputs that determine whether a vendor appears on an AI-generated shortlist, or disappears from consideration entirely.

Read the full article on Search Engine Journal

Author Bio

Prev

Prev